August 30, 2019

By Djalil Reghis and Nicolas Denjoy, Agroecology Capital

Download Agroecology Capital’s full report and investment thesis on indoor vertical farming, here. This report covers investment trends since 2010 and Agroecology Capital’s key investment drivers.

Food security, food quality, and resources scarcity are the main challenges the global agri-food system is facing. Indoor vertical farming promises to partially address these challenges by producing locally and efficiently fresh, chemical-free, and nutritious food. New farming systems increase yields, use less land and water, and allow a close quality and safety monitoring.

These promises and the ability of indoor vertical farming to industrialize high-value crop production have created a perfect window of opportunity to disrupt a multi-billion market (just for the U.S. leafy greens market), leading investors to respond favorably by investing large amounts in this industry.

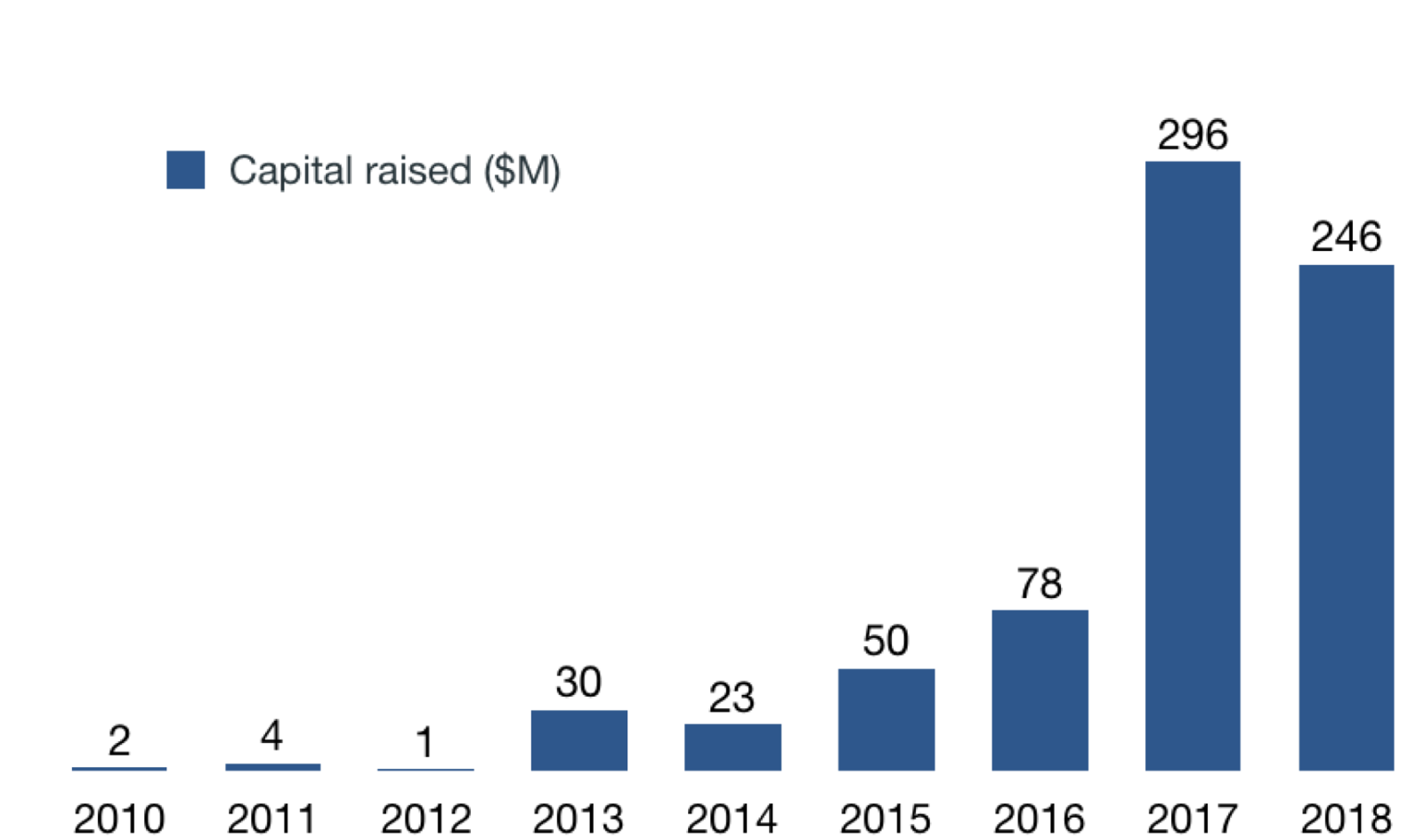

Venture capital investment in indoor vertical farming is getting a strong traction

To assess the magnitude of these investments, Agroecology Capital’s report listed publicly available deals in indoor vertical farming between 2010 and 2019, globally. This report narrowed the scope of the analysis to companies that have developed comprehensive growing solutions with a substantial innovation component. Thus, companies with stable technologies (i.e., conventional greenhouses) or that only produce components (i.e., LED lighting) have been excluded from the scope.

The selected deals comprehend 31 different startups that, collectively, have received $873 million between 2010 and 2019 (see the list of startups on the report).

Source: Agroecology Capital Research, 2019. Figures from Pitchbook, Crunchbase, CB Insights, and market data

Indoor vertical farming has represented a significant and increasing share of total AgTech venture capital investments. Large rounds such as AeroFarms (2013 and 2017) and Plenty ($200 million in 2017) led this vertical’s share to boost in 2013 and 2017 (10 percent in 2013 and 15 percent in 2017). Unsurprisingly, the U.S. has concentrated 89 percent of total investments between 2010 and 2019.

Despite a strong value proposition, several key aspects are still unclear from an investment perspective

Production costs for indoor vertical farming suffers when compared to conventional agriculture. Main production inputs, which are freely available in nature (i.e., light, air, water, CO2), have to be supplied at cost in indoor vertical farming. According to some startups, costs for an indoor-grown salad can reach twice those for an outdoor-grown one, putting energy efficiency[1] as a critical factor to optimize.

The high capital intensity required for scaling a vertical farming business is also a challenge for an industry that can neither compete on cost nor benefit from a network effect to establish pricing power. Moreover, the potential economies of scale are still unclear, if not insignificant. Although, energy prices might be subject to negotiation with energy suppliers, this case has not been witnessed yet given the small scale of current players.

Further, indoor vertical farms are currently able to grow only a limited number of crops. Leafy greens and herbs are easy to grow indoors, but other crops might be harder to grow at scale. The lack of readily available applied scientific research and data might also add risk on this vertical.

No player so far has proven that there is a sizable addressable market ready to pay more for a superior product or a product grown differently. The ability of the industry players to price discriminate might be a critical factor not only in reaching profitability but also in supporting an attractive business model.

Finally, there is no clear winner to date, and the range of current business models such as licensing technology and/or operating farms (the two main ones) might be a sign that the industry is still searching for an appropriate business model.

Venture Capital investment in indoor vertical farming: vertical integration vs. specialization

© Michael Sapryhin

Indoor vertical farming’s value chain might ultimately parallel that of traditional farming. Most of the value creation might be captured either by oligopolistic players at critical steps of the value chain (seeds bioengineering platforms, mass-market brand builders, and production technology providers) or by players with compelling business models.

Source: Agroecology Capital Research, 2019

Developing specific seeds for indoor vertical farming (i.e., optimized for Controlled Environment Agriculture and miniaturized crops) might lead to an improvement in yield and better-quality crops. Increasing crops variety, at an economically viable price, might also expand the addressable market. Startups focusing on seeds breeding and bioengineering for seeds adapted to indoor vertical farming might create attractive venture capital investment opportunities.

Demonstrating the outstanding quality of indoor-grown products will help to create strong brands and de-commoditize these products, which might constitute a category of their own. Price positioning indoor-grown products as premium goods will ultimately allow growing companies and retailers to capture a significant share of the value.

Full suite of proprietary technologies (hardware and software) could increase product quality, operations efficiency, and reduce production costs. Data will undoubtedly play a central role in increasing yields and stabilizing/optimizing production. However, growing a crop, unlike improving the performance of chips, do not obey Moore Law. Improvement of production technologies will in fine lead to marginal gains, and value might shift to hardware, software, and ultimately data.

Innovative business models might help solve the capital intensity challenge by outsourcing the capital expenditure required to build facilities. Franchise model, for instance, might allow players to focus their resources on their proprietary technologies (including seeds bioengineering) while having franchisees invest in building facilities.

“In a Gold Rush, Sell Shovels”

Indoor Vertical Farming delivers outstanding returns for consumers (food security, safety, and quality) and probably for the Planet (less water and chemicals use vs. increase in energy consumption?).

However, the industry still needs to demonstrate a clear path to profitability and scalability. In its search of this path, proprietary technology providers (seeds bioengineering and production technology) might play a prominent role while mass-market brand builders might establish a new premium food product category.

From an investment perspective, strong macro drivers are pulling investment toward this industry, which is currently vertically integrated. Investors might want to funnel their investments into more focused and specialized technology players mastering critical parts of the value chain. These players might offer the most promising investment returns by successfully applying the adage “In a Gold Rush, Sell Shovels.”

[1] Weight of product grown with a kWh of energy input.

. . .

Agroecology Capital is an AgTech VC fund based in Palo Alto, CA. The fund invests in early-stage technology ventures (Seeds and Series A) that help agriculture to transition toward practices focused on Safety, Sustainability, Productivity, and Equitability (Agroecology).

Djalil Reghis

Djalil is a co-founder and General Partner at Agroecology Capital. He has 12 years of experience in consumer-packaged goods, investment, M&A, government affairs, and served as a Board Director at Emiral. Djalil has been in the agri-food industry for the last seven years. He graduated from the Stanford Graduate School of Business.

Nicolas Denjoy

Nicolas is a co-founder and General Partner at Agroecology Capital. Nicolas has been an entrepreneur and investor in the agribusiness and the technology sectors for nearly 20 years. He served as a board member of Agrogeneration (listed FR:ALAGR), a 240.000 acres farm located in Ukraine. Nicolas graduated from the Stanford Graduate School of Business.

Let GAI News inform your engagement in the agriculture sector.

GAI News provides crucial and timely news and insight to help you stay ahead of critical agricultural trends through free delivery of two weekly newsletters, Ag Investing Weekly and AgTech Intel.