By Weiyi Zhang, Ph.D., Senior Agricultural Economist, Manulife Investment Management

A blast from the past—or is it?

— Inflationary pressures are expected to weigh on farmers’ financial profitability, but commodity prices remain at historically high levels.

— Farmland can demonstrate stable and resilient return performance through periods of differing economic cycles.

— The changing interest-rate environments and pronounced market volatility of past decades have encouraged investor interest in low-risk, income-generating asset classes.

Wading Through a New Era: Pent-up Inflationary Pressures as Monetary Policies Tighten

The global economy and financial markets have experienced significant volatility over the past few months, with inflationary pressures heightened and monetary policies beginning to tighten. During January and February 2022, U.S. consumer price-level increases accelerated to their highest level in 40 years, posting 7.5 percent and 7.9 percent in year-over-year changes in the Consumer Price Index (CPI) for two consecutive months. Core CPI readings, after excluding volatile cost components such as food and energy, also increased at an annual rate of 6.4 percent in February 2022. The current heated state of the economy has pushed the U.S. Federal Reserve (Fed) to end the near-zero interest-rate environment by raising interest rates for the first time since 2018. Fueled by additional risk factors, such as regional geopolitical conflicts, higher inflation and more interest-rate hikes are expected.

Current inflation hits a 40-year high, yet remains far below its previous peak

Monthly change in CPI and Core CPI from the previous year

Source: FRED, as of March 10, 2022. CPI refers to the Consumer Price Index. YoY refers to year over year.

Source: FRED, as of March 10, 2022. CPI refers to the Consumer Price Index. YoY refers to year over year.

In these uncertain times, we should take a historical perspective of the relationship between farmland returns, inflation, and interest rates in order to look forward.

The Fed raised the interest rate in March 2022

Daily U.S. federal funds effective rate

Source: FRED, as of March 23, 2022.

Farmland Investments Generating Real and Healthy Returns: A Historical Review

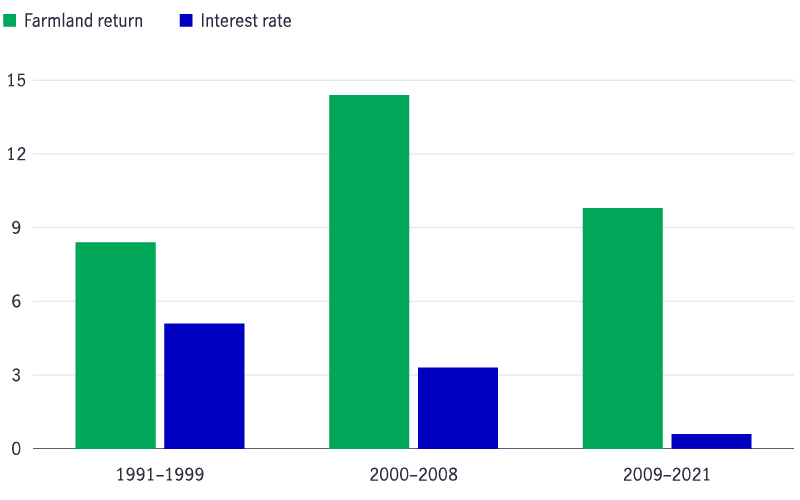

Farmland as an asset class has attracted investors’ attention for the last three decades. The National Council of Real Estate Investment Fiduciaries (NCREIF) Farmland Index (NFI) was first synthesized to measure the investment performance of privately owned and managed farmland properties in the United States, and is widely considered an appropriate proxy for U.S. farmland investment returns. Since the NFI’s inception in 1991, U.S. farmland has generated an average annual return of 10.7 percent, on par with the average performance of the U.S. and international stock markets, represented by the average annual returns of the S&P 500 Index at 12.6 percent and the MSCI World Index at 8.0 percent during the same period.1 Farmland also exhibited consistent performance during differing periods in the past three decades, delivering 8.4 percent per year during the pre-dot-com years (1991–1999), 14.4 percent per year leading into the Great Financial Crisis (GFC) (2000–2008), and 9.8 percent per year during the protracted recovery period post-GFC (2009–2021). Compared against the average inflation rate of 2.4 percent per year in the past 30 years, farmland’s average performance provided investors with healthy real returns.

Farmland investments have generated positive returns over contrasting periods since 1991

NCREIF Farmland Index average returns (%)

Source: NCREIF Farmland Index, as of December 31, 2021.

Source: NCREIF Farmland Index, as of December 31, 2021.

Investors look for an additional return over inflation in asset classes to protect their investment returns from inflationary pressure, and farmland has historically been regarded as a suitable inflation hedge. Farmland returns have generally moved in the same direction as inflation rates, represented by a mild 0.06 historical correlation between NFI returns and CPI inflation rates from 1991 through 2021.

Farmland returns have positively correlated with inflation historically

Correlation between the NCREIF Farmland Index and CPI inflation by period

Source: NCREIF Farmland Index, as of December 31, 2021.

The sub-periodic correlation between farmland and inflation sheds light on the relationship between farmland returns and inflation rates. During the first two periods (1991–1999 and 2000–2008), farmland returns correlated positively with inflation, with correlation coefficients at 0.20 and 0.28, respectively. During these two periods, farmland was generating healthy returns while the economy was expanding at a robust pace, with CPI inflation above 2.5 percent per year. Turning to the post-GFC period (2009–2021), this correlation turned negative, dampening the overall correlation pattern during the entire NFI period.

The Dynamic Correlation Patterns Between Farmland Returns and Inflation Rates

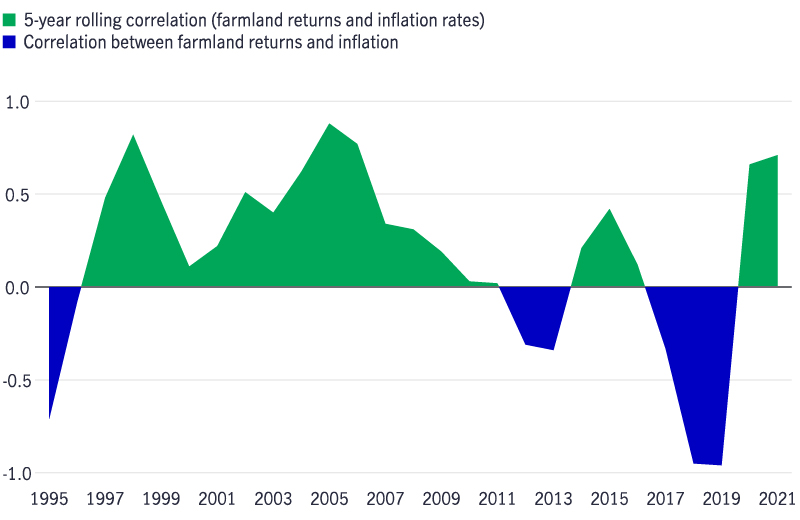

The correlation between farmland and inflation presents a dynamic pattern throughout history, demonstrated by rolling correlation analysis. While the correlation was mostly positive on a rolling basis, during some yearly periods, it broke pattern and turned negative (e.g., during the post-GFC period).

The correlation between farmland returns and inflation shows a dynamic pattern with positive overtones

NCREIF Farmland Index returns vs. CPI inflation rates

Source: FRED, as of March 10, 2022. CPI refers to the Consumer Price Index.

The overall negative correlation of 2009 through 2021 and the negative rolling correlation of two instances in this period could be attributed to the different directions taken by farmland returns and inflation rates. The economic recovery post-GFC was considered lackluster, with 7 of the past 13 years posting inflation below the desired 2 percent target. Meanwhile, farmland gained significantly during the same period, especially from 2011 to 2015, when the NFI posted double-digit percentage returns for five consecutive years. The difference between the robust performance of farmland against the flattened economic expansion contributed to the negative correlation in the period and lowered the overall positive correlation from 1991 to 2021. Therefore, from the investor’s perspective, a negative correlation may represent an asset class’s ability to outperform otherwise lukewarm growth in the broader economy when the inflation rate is below target.

Comparing Previous High Inflation with the Current Environment

Comparing the previous period of high inflation with the current one, we can study the similarities, or differences, in inflation causes and examine their potential impact on asset returns. The previous period of high inflation was from 1979 to 1981, when CPI annual changes averaged 11.7 percent. Attributes that contributed to rising inflation rates during that period and those contributing to current inflation are different: today, the leading inflationary components by far are gas prices and used vehicles and utilities, driven by rising energy prices and supply chain disruptions, which exert outsize pulling effects on the inflation rate. In contrast, inflationary changes were spread more broadly between a wide variety of components during the previous inflation period, spanning energy sectors, commodities, and food items.

Energy and supply chain issues have outsize effects on current inflation

CPI increase for select cost components, 1979–1981 (average) and 2021 (%)

Source: Macrobond, as of March 15, 2022.

Rising Inflation and its Potential Impact

Rising inflationary pressures are expected to weigh on farmers’ financial profitability in the coming year. The U.S. Department of Agriculture’s forecast costs of production for corn and soybeans for the crop year 2022 show higher expenses in fuel and energy inputs (7.4 percent), chemical inputs (6.3 percent), and fertilizer costs (9.5 percent). Of the total costs of production, these three expense categories combined to account for 59 percent of corn production costs and 47 percent of soybean production costs in 2020. Adding to the uncertainty, fertilizer costs are expected to climb higher due to Russia’s invasion of Ukraine and the fact that Russia is a major fertilizer exporter. On the flip side, while forecast costs are at all-time highs, commodity prices also remain at historically high levels: cushioning rising costs, high commodity prices, and increased acreage are expected to absorb some of the negative impacts, leaving operators with relatively healthy margins.

Production expenses will increase, driven by higher costs for fuel, fertilizers, and chemicals

Production cost increase for U.S. corn and soybeans, 2020–2022 (% forecast)

Source: Macrobond, as of March 15, 2022.

Evolving Over the Years: The Interaction Between Interest Rates and Farmland Returns

Interest rates are expected to see several hikes in the United States in 2022 and 2023, until the federal funds rate reaches 2 percent by the end of 2023. The relationship between interest rates and farmland returns is intricate and evolves over time, and there doesn’t seem to be a linear relationship between the two when examining the average rates by period: When interest rates lowered from an average of 5.1 percent in the 1991 to 1999 period to 3.3 percent in the period from 2000 to 2008, farmland returns in the NFI grew 6 percent higher on an annual basis, from 8.4 percent per year to 14.4 percent, respectively. However, transitioning into the post-GFC period (2009–2021), both interest rates and farmland returns decline on an annual average basis.

The uneven relationship between interest rates and farmland returns

Periodic average NCREIF Farmland Index returns and interest rates (%)

Source: FRED, as of March 23, 2022.

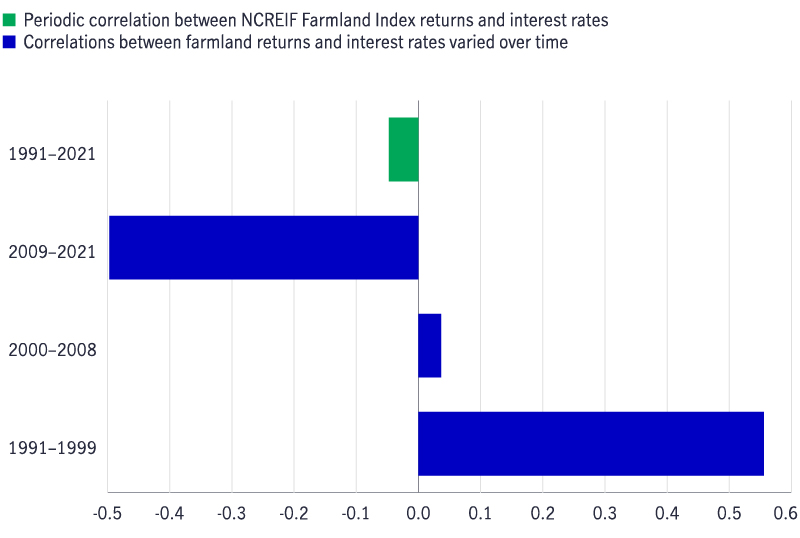

Dissecting return data into periods as previously defined, these correlation patterns also affirm the inconsistent correlation between farmland returns and interest rates. While the overall correlation between 1991 and 2021 was mildly negative at –0.05, it was augmented by the significantly negative correlation seen during the post-GFC period at –0.50. Effective fund rates compressed to near zero during the post-GFC period as the Fed stayed committed to extremely accommodative monetary policies while farmland soared on strong demand for farm goods and farmland. The lack of a consistent farmland return response to interest-rate swings demonstrates farmland’s stable and resilient return performance through periods of differing economic cycles.

The correlation between farmland returns and interest rates has varied over time

NCREIF Farmland Index returns and interest rates

Source: FRED, as of March 23, 2022.

Increasing interest rates can often be associated with lower asset values; nevertheless, other factors also contribute to changes in asset valuations, especially for farmland values. Comparing average interest-rate levels and NFI appreciations, measured by five-year rolling average values, the pattern shows interesting deviations from its theoretical negative associations. On the one hand, there were periods during which interest rates and farmland appreciation rates trended with an inverse relationship, as seen in the 2011 to 2019 period. On the other hand, there were periods during which interest rates and appreciation rates trended together. During the 2004 to 2010 period, for example, five-year rolling average interest and appreciation rates moved in similar directions. These observations, which depart from orthodox theory, suggest that there are other factors in determining land appreciation.

The relationship between farmland appreciation and interest rates is mixed

Five-year rolling average interest rates and NCREIF Farmland Index appreciation rates

Source: FRED, as of March 23, 2022.

The farmland market works on fundamental economic concepts of supply and demand: when interest in farmland as an asset class increases, the value of farmland assets tends to elevate. A comparison between five-year rolling average interest rates and NFI property counts reaffirms increasing investor interest in farmland. While average interest rates have decreased from a range of 4 to 5 percent in the 1990s until bottoming out shortly after the GFC, the number of properties within the NFI has increased more than sixfold since inception, from 197 at the end of 1991 to 1,260 in Q4 2021. The changing interest-rate environments and pronounced market volatility of the past three decades have helped encourage investors to seek out low-risk, income-generating asset classes.

Institutional interest in farmland has increased

Five-year rolling average interest rates and NCREIF Farmland Index property counts

Source: FRED, as of March 23, 2022.

The New Era of Elevated Inflation and a Changing Monetary Environment: Farmland’s Promising Outlook Despite Near-term Challenges

The near-term impact of inflation and regional geopolitical risks is expected to affect farm production and profitability. Increasing costs for key agricultural production inputs, such as fertilizers, fuel, and energy, are expected to weigh on agricultural financial bottom lines, which can be partially offset by high crop prices and improving supply chain situations. Overall, while inflationary pressure has built up, farmland has historically provided investors with protection from inflation. Farmland can provide investors with real returns over inflation rates, represented by the positive correlation with CPI seen during the 1991 to 2008 period. In addition, low inflation rate periods, such as the post-GFC period when farmland returns correlated negatively with inflation, saw farmland continue to deliver healthy returns for investors. Farmland also is expected to maintain its positive momentum despite the federal funds rate being predicted to reach 2 percent by the end of 2023. Historical performance has shown that interest-rate environments alone have not single-handedly determined farmland returns and that interest in the asset class has been upbeat under various interest-rate levels. 2

Going forward, farmland continues to represent an attractive asset class. Investors’ increasing emphasis on non-financial goals, such as the environmental and social aspects of their investments, creates a new tier for farmland demand: as agricultural production integrates with technological innovations, agriculture can play a key role as a natural climate solution, providing additional opportunities for farmland investors and injecting new enthusiasm for farmland in the new era.

NOTES:

[1] Macrobond, as of March 1, 2022

[2] Past performance does not guarantee future results.

ABOUT THE AUTHOR

Weiyi Zhang, Ph.D. is a senior agricultural economist with Manulife Investment Management. In this role, he conducts economic research to support the firm’s business and agricultural investment decisions, and is directly involved in farmland transactional due diligence and initiating new investment strategies and concepts. In addition, he is responsible for the global agricultural economic, financial, and statistical analytical efforts, including commodity price forecasting, portfolio analysis, and authoring thought leadership publications. Previously, Zhang was the senior natural resource economist, where he supported economic research and analysis for the group’s timberland and farmland business sectors. He holds a bachelor of science in agricultural and applied economics, a master of forest resources (M.F.R.), and a Ph.D. in forest finance and economics.

Weiyi Zhang, Ph.D. is a senior agricultural economist with Manulife Investment Management. In this role, he conducts economic research to support the firm’s business and agricultural investment decisions, and is directly involved in farmland transactional due diligence and initiating new investment strategies and concepts. In addition, he is responsible for the global agricultural economic, financial, and statistical analytical efforts, including commodity price forecasting, portfolio analysis, and authoring thought leadership publications. Previously, Zhang was the senior natural resource economist, where he supported economic research and analysis for the group’s timberland and farmland business sectors. He holds a bachelor of science in agricultural and applied economics, a master of forest resources (M.F.R.), and a Ph.D. in forest finance and economics.

Important disclosures

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange-trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other preexisting political, social, and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or its affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment or legal advice. This material was prepared solely for informational purposes, does not constitute a recommendation, professional advice, an offer or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or protect against the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional.

Australia: Manulife Investment Management Timberland and Agriculture (Australasia) Pty Ltd, Manulife Investment Management (Hong Kong) Limited. Canada: Manulife Investment Management Limited, Manulife Investment Management Distributors Inc., Manulife Investment Management (North America) Limited, Manulife Investment Management Private Markets (Canada) Corp. China: Manulife Overseas Investment Fund Management (Shanghai) Limited Company. European Economic Area Manulife Investment Management (Ireland) Ltd. which is authorised and regulated by the Central Bank of Ireland Hong Kong: Manulife Investment Management (Hong Kong) Limited. Indonesia: PT Manulife Aset Manajemen Indonesia. Japan: Manulife Investment Management (Japan) Limited. Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U) Philippines: Manulife Investment Management and Trust Corporation. Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G) South Korea: Manulife Investment Management (Hong Kong) Limited. Switzerland: Manulife IM (Switzerland) LLC. Taiwan: Manulife Investment Management (Taiwan) Co. Ltd. United Kingdom: Manulife Investment Management (Europe) Ltd. which is authorised and regulated by the Financial Conduct Authority United States: John Hancock Investment Management LLC, Manulife Investment Management (US) LLC, Manulife Investment Management Private Markets (US) LLC and Manulife Investment Management Timberland and Agriculture Inc. Vietnam: Manulife Investment Fund Management (Vietnam) Company Limited.

Manulife, Manulife Investment Management, Stylized M Design, and Manulife Investment Management & Stylized M Design are trademarks of The Manufacturers Life Insurance Company and are used by it, and by its affiliates under license.

551638

*The content put forth by Global AgInvesting News and its parent company HighQuest Partners is intended to be used and must be used for informational purposes only. All information or other material herein is not to be construed as legal, tax, investment, financial, or other advice. Global AgInvesting and HighQuest Partners are not a fiduciary in any manner, and the reader assumes the sole responsibility of evaluating the merits and risks associated with the use of any information or other content on this site.